|

|

Healthcare.gov - Nov. 30th; Define Success (Page 2)

|

|

|

|

|

Professional Poster

Join Date: Dec 2006

Location: Maryland

Status:

Offline

|

|

OAW,

Thank you for quoting the Administration's talking points on the ACA.

I'm looking for reality, not the Administration's PR machine.

The consumer protections can remain without the rest of the ACA. That they're bundled doesn't justify the rest of the law (we can keep those without needing to upend the entire industry).

We've seen several reports from reputable sources that premiums are going up, less people are covered, jobs are disappearing and small business's are being squeezed to cover the new entitlement. What do we have to show for it?

I'm looking for [i]actual positive results[/] from the ACA to date, from sources other than the Administration itself and it's satellite organizations. You've provided Administration PR talking points which have been repeatedly refuted and severely undermined by independent, credible sources.

Show me one area that the ACA has actually made good on it's promises. We all know what the Admin promised and we all know to date how credible those promises are. Give me something real.

|

|

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Apr 2003

Location: 46 & 2

Status:

Offline

|

|

Originally Posted by turtle777

WTF, OAW ?

-t

Bury the opposing side under a mountain of partial-truths and rhetoric, crafted the make them think, "screw it, whatever". You know the drill.

|

|

"Those who expect to reap the blessings of freedom must, like men, undergo the fatigue of supporting it."

- Thomas Paine

|

| |

|

|

|

|

|

|

|

Addicted to MacNN

Join Date: May 2001

Status:

Offline

|

|

Originally Posted by ebuddy

We have to wait for the law to find out what's in it. Sounds familiar.

Actually we know what's in it. The Employer Mandate doesn't take effect until 2015. So again, trying to make the argument that jobs are being eliminated due to a provision that's not even in effect yet is dubious at best.

Originally Posted by WSJ quote

:

Public Opinion Strategies survey of more than 400 business owners with between 40 and 500 employees conducted in September and October for the U.S. Chamber of Commerce and International Franchise Association. Some 64% of small business franchise owners (such as owners of fast food and retail stores) believe the law will have a "negative impact" on their business, while only 5% expect a "positive impact." For non-franchise businesses the ratio was 53% negative and 12% positive. Only one in 12 agree with the President that the health-care law will "help" their business.

Love how you are trying to characterize the entire ACA based on a survey of 400 business owners that are all in the franchise game. As if that's a broad cross-section of American business.

Originally Posted by WSJ quote

The survey also reveals that the "49er" effect is very real. These are businesses that will cap their full-time payroll workforce at 49 employees to avoid ObamaCare's insurance mandate for companies with more than 50 full-time equivalent workers. Of firms with between 40 and 70 employees, a little over half say they are likely to "make personnel decisions to keep" their "workforce below the threshold of 50 full-time employees and avoid the requirements and penalties associated with the new health care law."

As if US businesses don't ALREADY steer employees into part-time positions to avoid paying them benefits. REGARDLESS of the ACA. The largest private employer in the country Wal-mart is NOTORIOUS for doing this. Furthermore, small businesses are often exempt from a variety of regulations that are imposed on their larger counterparts. So the "49er effect" exists for non-ACA regulations too. And yet we've still managed to create the largest economy on the planet and the sky has yet to fall. ")

Regarding your objection to the "Cadillac Tax", weren't you the same guy who recently said this?

Originally Posted by ebuddy

And the reason they [healthcare providers] can is because they're not charging you, they're charging Blue Cross Blue Shield or the Federal Government. They're also required to carry preposterous insurances and comply with a wealth of other regulations both State and Federal. This is what happens in a distorted marketplace. What the story missed was; Then the bills arrived. Ms. Singh’s three stitches cost $2,229.11 of which she was expected to pay about $450.00.

And this?

Originally Posted by ebuddy

Health care providers charge what they do because they're not subjected to normal market forces. After all, they're not really charging you, they're charging monolithic corporations. The monolithic corporation could be ACMECORP or GOVT, it really doesn't matter. Unless this changes, health care costs will continue to increase. Health care insurers charge premiums that enable voluminous clientele and a meager profit margin they can roll into much more lucrative ventures.

And this isn't a newfound position that you've advocated. You've long promoted the view that the reason why healthcare costs continue to skyrocket is because the consumer is shielded from the true cost. And while that idea has merit I've quibbled with you about whether that's the only reason. That being said, the "Cadillac Tax" is a provision of the ACA specifically designed to address that issue. It certainly doesn't implement the "insurance for catastrophic events only and HSA 's and cash payments for everything else" approach that you advocate. Quite frankly, that's an approach that would be even more "radical" with respect to the amount of change it would entail than going with a Single Payer health insurance system. Nonetheless, it does take a significant step in that direction. Yet, now you oppose it. Hmmm.

In any event, that's a provision not set to take effect until 2018.

Originally Posted by ebuddy

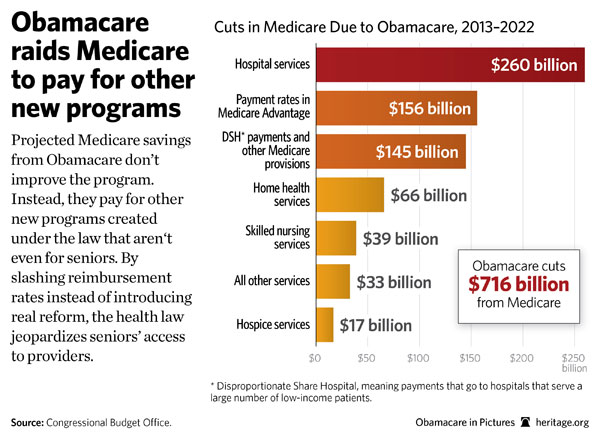

You mean the same $716 billion supported by Romney and the House GOP voted for in the Ryan budget? The same amount that fact checkers have UNIVERSALLY called the GOP "disingenuous" at best when they criticize Obama about it? Again, it's cool when they GOP advocates it. But it magically becomes a problem when a Dem promotes the exact same thing. Is anyone else noticing a pattern here?

Paul Ryan said President Obama “funneled” $716 billion out of Medicare “at the expense of the elderly.” | PolitiFact

FACT CHECK: Obama, Ryan, Romney Backed Medicare Cuts - ABC News

Medicare’s ‘Piggy Bank’

Originally Posted by ebuddy

Let's expand an already woefully insolvent program. Only an ideological progressive could come up with something so dubious.

I'll just direct you to what the CBO had to say about that ...

When estimates are compared on a year-by-year basis, CBO and JCT’s estimate of the net budgetary impact of the ACA’s insurance coverage provisions has changed little since February 2013 and, indeed, has changed little since the legislation was being considered in March 2010. In March 2010, CBO and JCT projected that the provisions of the ACA related to health insurance coverage would cost the federal government $759 billion during fiscal years 2014 through 2019 (which was the last year in the 10-year budget window being used at that time). The newest projections indicate that those provisions will cost $710 billion over that same period. As shown in the figure below, the intervening projections of the cost of the ACA’s coverage provisions for those years have all been close to those figures on a year-by-year basis; of course, the 10-year totals have changed as the time frame for the estimates has shifted.

Those amounts do not reflect the total budgetary impact of the ACA. That legislation includes many other provisions that, on net, will reduce budget deficits. Taking the coverage provisions and other provisions together, CBO and JCT have estimated that the ACA will reduce deficits over the next 10 years and in the subsequent decade.

CBO | CBO’s Estimate of the Net Budgetary Impact of the Affordable Care Act’s Health Insurance Coverage Provisions Has Not Changed Much Over Time

Originally Posted by ebuddy

Heavily subsidized on the backs of the young and healthy.

As is health insurance in general.

Originally Posted by ebuddy

An element of the law the President had to outright lie about for passage.

The Obama Administration has been quite up front about the need to have young people sign up in order to make popular provisions like "No denial for pre-existing conditions" feasible. The individual mandate is the lynchpin to make the healthcare exchange work in what is fundamentally a private insurance based system. Which is precisely why the GOP supported it .... until it was implemented by a Dem. Hmmm ... there we go with that pattern thing again.

Originally Posted by ebuddy

Given that this has been called the Affordable Care Act, I'm not interested in the .gov's actual name for the fee. Employers aren't untouched. Trust me. It'll be yet another "I told you so" moment that you and MSNBC will be trying to spin again later this year and next.

We shall see.

Originally Posted by ebuddy

Let's see here, should I take the words of OAW, the Obama Administration, and MSNBC or should I take the words of the overwhelming majority of small businesses and the SBA representing them in ardently opposing the ACA? I'm sorry. It is going to be yet another "I told you so" moment for Republicans and blue-dog Dems now running from it and this Administration.

"Overwhelming majority of small businesses" based on what? That little poll of 400 business owners that are all in the franchise game you mentioned?

Originally Posted by ebuddy

I like how you immediately start by bloating the number of uninsured. That's rich. Is that the number of uninsureds since Obamacare was implemented?

I didn't bloat anything. If you don't like the figure take it up with the Washington Post.

Originally Posted by ebuddy

I stand corrected. The proper statement would've been; little more than a third. But that's splitting hairs of course.

Well it appears that I'm going to have to correct you again. let's review your original statement:

Originally Posted by ebuddy

We've upended the entire health care industry to cover one-third [of] the uninsured when it's all said and done.

Now that's what YOU said. But what the numbers show is ...

- 54 million uninsured in 2010.

- ACA insures 32 million of those by 2019.

- Leaving 22 million uninsured in 2019.

32/54 = 0.5925925926

So we are looking at covering approximately 60% of the uninsured. I think that qualifies as substantially more than a " little more than a third".

Originally Posted by ebuddy

With all due respect, this is among the most ignorant things I've read in this forum in a very long time and so illustrative of the problem in politics today. There is absolutely no possible meat on the bone for reason here. Zero. The ACA dropped a bunker-buster on an anthill. By design. Period. End of story. Please spare me your lecture on what you believe the GOP does or does not care about. They are a party of folks that dollar-for-dollar, give more. Substantially more.

- Nicholas D. Kristof, NYT

“When I started doing research on charity,” Mr. Brooks; author of a book on donors to charity, “Who Really Cares” wrote, “I expected to find that political liberals — who, I believed, genuinely cared more about others than conservatives did — would turn out to be the most privately charitable people. So when my early findings led me to the opposite conclusion, I assumed I had made some sort of technical error. I re-ran analyses. I got new data. Nothing worked. In the end, I had no option but to change my views.”

It's a much more fundamental difference in views that has nothing to do with one lacking in compassion for another.

From your own article ....

When liberals see the data on giving, they tend to protest that conservatives look good only because they shower dollars on churches — that a fair amount of that money isn’t helping the poor, but simply constructing lavish spires.

It’s true that religion is the essential reason conservatives give more, and religious liberals are as generous as religious conservatives. Among the stingiest of the stingy are secular conservatives.

According to Google’s figures, if donations to all religious organizations are excluded, liberals give slightly more to charity than conservatives do.

In any event, the characterizations I made in silver above ... admittedly exaggerated a smudge for for the sake of humor ... are views that are ROUTINELY expressed by conservatives. Often in this very forum.

Originally Posted by ebuddy

Originally Posted by OAW

There is an old adage .... "Don't let the perfect be the enemy of the good." Perhaps one day our good friends on the right will take heed to that wisdom with respect to the ACA.

I think the more apt adage here is; "The road to hell is paved with good intentions." There are those expecting perfection, you won't find them on the right. They already know better.

And THAT my friend is one helluva repartee! Which is why I always enjoy our debates.

OAW

|

|

|

| |

|

|

|

|

|

|

|

Addicted to MacNN

Join Date: May 2001

Status:

Offline

|

|

Originally Posted by Snow-i

OAW,

Thank you for quoting the Administration's talking points on the ACA.

I'm looking for reality, not the Administration's PR machine.

The consumer protections can remain without the rest of the ACA. That they're bundled doesn't justify the rest of the law (we can keep those without needing to upend the entire industry).

I appreciate your thoughtful response. So let's roll with that. You said the "Consumer Protections" can stay. That would be these ...

- Putting Information for Consumers Online.

- Prohibiting Denying Coverage of Children Based on Pre-Existing Conditions.

- Prohibiting Insurance Companies from Rescinding Coverage.

- Eliminating Lifetime Limits on Insurance Coverage.

- Regulating Annual Limits on Insurance Coverage.

- Appealing Insurance Company Decisions.

- Establishing Consumer Assistance Programs in the States.

- Prohibiting Discrimination Due to Pre-Existing Conditions or Gender.

- Eliminating Annual Limits on Insurance Coverage.

- Ensuring Coverage for Individuals Participating in Clinical Trials.

So how exactly would one provide these consumer protections ... especially the popular key provisions in blue ... without the individual and employer mandates for example that make such things feasible?

Originally Posted by Snow-i

We've seen several reports from reputable sources that premiums are going up, less people are covered, jobs are disappearing and small business's are being squeezed to cover the new entitlement. What do we have to show for it?

- Premiums have been going up for decades. Often at double-digit rates. The rate of increase has actually slowed since the ACA was passed.

- It's dubious that less people are covered. Some in the individual market who purchased plans after the ACA was passed that didn't meet the new coverage standards had their policies cancelled. The "grandfather clause" only applied to those that existed prior to the law's passage. Which IMO was a mistake. It should have covered such policies until the the open enrollment period began for the Healthcare Exchange. In any event, most of those people will get a new, more comprehensive policy on the exchange. You know ... something that actually covers things like hospitalization or medical procedures. Additionally, the Obama Administration extended the grandfathering period (subject to state insurance regulatory approval) for those affected policies. Then we have the millions that have signed up on the Exchange since the website was fixed. A number that is only sure to grow exponentially as the end of the open enrollment period approaches.

- Jobs are disappearing based on what? Certainly not in the aggregate ....

- Small businesses are specifically exempt from the employer mandate provisions of the ACA.

Originally Posted by Snow-i

I'm looking for [i]actual positive results[/] from the ACA to date, from sources other than the Administration itself and it's satellite organizations. You've provided Administration PR talking points which have been repeatedly refuted and severely undermined by independent, credible sources.

Show me one area that the ACA has actually made good on it's promises. We all know what the Admin promised and we all know to date how credible those promises are. Give me something real.

I showed you mine ... now show me yours. IOW, I listed those aspects of the ACA that are already in effect. You say they've "been repeatedly refuted and severely undermined by independent, credible sources". So take some of the provisions I listed and then provide such sources that do so. I don't mean sources that are PREDICTING the sky falling at some point because of those provisions. I mean sources that demonstrate that those provisions are NOT actually in effect as the Obama Administration has claimed.

OAW

|

|

|

| |

|

|

|

|

|

|

|

Addicted to MacNN

Join Date: May 2001

Status:

Offline

|

|

Originally Posted by Shaddim

Originally Posted by turtle777

WTF, OAW ?

-t

Bury the opposing side under a mountain of partial-truths and rhetoric the actual source material (e.g. the CBO Report), crafted the make them think, "screw it, whatever". You know the drill.

Only the intellectually lazy, "tl/dr" crowd would think "screw it, whatever". And for whom the shoe fits ...

OAW

PS: And how would you know what I said anyway? Weren't you supposed to have put me on "ignore"? But since you obviously didn't ... don't think I forgot about that bit of "proof" that's still lacking.

|

|

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Jun 2001

Location: planning a comeback !

Status:

Offline

|

|

Originally Posted by OAW

Only the intellectually lazy, "tl/dr" crowd would think "screw it, whatever". And for whom the shoe fits ...

So, you think the hole "we have to pass it to find out what's in it" thing was the intellectually honest thing to do ?

Methinks the reason was more than just keeping the "lazy" at bay.

BUT: there are always people like you who will get a hard on from thousands of pages of bullish!t.

-t

|

|

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Apr 2003

Location: 46 & 2

Status:

Offline

|

|

Originally Posted by OAW

Only the intellectually lazy, "tl/dr" crowd would think "screw it, whatever". And for whom the shoe fits ...

OAW

PS: And how would you know what I said anyway? Weren't you supposed to have put me on "ignore"? But since you obviously didn't ... don't think I forgot about that bit of "proof" that's still lacking.

I tried to give you another chance, after 3 weeks on ignore, that was a mistake it seems. I linked the phrase but you brushed it off, I explained the rest, but that wasn't good enough and you wanted blood. Then you decided to bring my family into it. What the f*ck is wrong with you? Is it my turn to start saying things about your wife? Your kids? At what point are you going to realize the friction in this (the walking on glass feeling in the PWL) is from your own temper?

|

|

"Those who expect to reap the blessings of freedom must, like men, undergo the fatigue of supporting it."

- Thomas Paine

|

| |

|

|

|

|

|

|

|

Posting Junkie

Join Date: Aug 2003

Location: midwest

Status:

Offline

|

|

Originally Posted by OAW

Actually we know what's in it. The Employer Mandate doesn't take effect until 2015. * So again, trying to make the argument that jobs are being eliminated due to a provision that's not even in effect yet is dubious at best.

*2015 as determined in July of 2013, just 5 months before the mandate would've otherwise kicked into play. The point is, I don't have to wonder if businesses will respond this way in 2015, OAW, they've already begun.

Love how you are trying to characterize the entire ACA based on a survey of 400 business owners that are all in the franchise game. As if that's a broad cross-section of American business.

You may have missed the latter half of the info I cited. For non-franchise businesses the ratio was 53% negative and 12% positive. Only one in 12 agree with the President that the health-care law will "help" their business.

They're the ones with the most at stake OAW. I'm afraid we're just going to be at an impasse here.

As if US businesses don't ALREADY steer employees into part-time positions to avoid paying them benefits. REGARDLESS of the ACA. The largest private employer in the country Wal-mart is NOTORIOUS for doing this. Furthermore, small businesses are often exempt from a variety of regulations that are imposed on their larger counterparts. So the "49er effect" exists for non-ACA regulations too. And yet we've still managed to create the largest economy on the planet and the sky has yet to fall.

It's not about whether or not this element exists in the labor market, OAW; it's the apparent trends in the data and what we see in undesirable growth in the number of those leaving the market accompanied by increasing part-time employment. Sure, it could be deemed purely coincidental depending on whether or not the purveyor of the misfortune is a (R) or (D), but I'm trying to be less cynical than that.

What you must ignore: - “11.4%: What the U.S. unemployment rate would be if labor force participation were back to January 2008 levels.” …James Pethokoukis, American Enterprise Institute, June 2013

- “Over the last six months, of the net job creation, 97 percent of that is part-time work,”…Keith Hall, former BLS chief

Regarding your objection to the "Cadillac Tax", weren't you the same guy who recently said this?

How is it inconsistent that I'd make the case against government distortion of the marketplace using multiple perspectives? Providers have to stack up on insurance from mandates and regulation which then get passed to someone else -- the larger entities with the purse strings. Now that burden has been broadened in scope to encompass us all. Employers trying to do something nice for their employees now have to reconsider and people with great insurance plans now have to pay more for them, not because the employer or insurance company has deemed it so, but because the Federal government now picks and chooses preferred coverage options and adds a "luxury" tax of sorts on people's health care coverage. It's BS.

And this isn't a newfound position that you've advocated. You've long promoted the view that the reason why healthcare costs continue to skyrocket is because the consumer is shielded from the true cost. And while that idea has merit I've quibbled with you about whether that's the only reason. That being said, the "Cadillac Tax" is a provision of the ACA specifically designed to address that issue. It certainly doesn't implement the "insurance for catastrophic events only and HSA 's and cash payments for everything else" approach that you advocate. Quite frankly, that's an approach that would be even more "radical" with respect to the amount of change it would entail than going with a Single Payer health insurance system. Nonetheless, it does take a significant step in that direction. Yet, now you oppose it. Hmmm.

I oppose a government distortion of the marketplace. Government charging people a tax for a level of health care coverage has absolutely nothing to do with the health care provider and will do absolutely nothing to curb provider rates or waste, fraud, and abuse. This is you and too many Democrats quite frankly, continuing to confuse coverage with care.

In any event, that's a provision not set to take effect until 2018.

So... we'll wait for 2018 right Nancy OAW?

Of course, nowhere near "the same" cuts.

Fact-Checking the Obama Campaign's defense of its $716 billion cut to Medicare

Yuval Levin calls this the “Ryan did it too” defense. It has the merits of being factually accurate, up to a point. As I discussed on Tuesday, it’s true that the House GOP budget preserved Obamacare’s Medicare cuts. But it’s hard to see how “Ryan did it too” allows Democrats to say that Ryan is throwing granny over a cliff, unless they are confessing guilt to the same crime.

There are two other points to bear on this subject. The first is that Ryan’s Medicare cuts were solely used to extend the solvency of the Medicare trust fund, and not to fund new spending elsewhere. By contrast, Obamacare cut $716 billion from Medicare in order to fund $1.9 trillion in new health care spending, through the law’s expansion of Medicaid and its new subsidized exchanges.

Decoding the $716 Billion in Medicare Reduction

a fellow at the Ethics and Public Policy Center said it was an "oversimplification" to say that Ryan was keeping the Obama Medicare cuts. "Ryan's budget allows the substitution of sensible ways of saving money in Medicare for the arbitrary and harmful cuts contained in Obamacare," he writes.

Forbes.com

One isn't bipartisan:

Obamacare emphasizes government control and central planning. The law empowers a panel of 15 unelected government officials, called the Independent Payment Advisory Board, to make changes to the Medicare program that will reduce Medicare spending: primarily paying doctors and hospitals less, as is done with the Medicaid program. Over time, liberal health-policy types hope that IPAB can be used to introduce rationing into Medicare, using the panel to determine what types of procedures and treatments that Medicare will and will not pay for.

One is:

The Wyden-Ryan plan, co-authored by liberal Sen. Ron Wyden (D., Ore.) and Paul Ryan, preserves the Obamacare targets for future Medicare spending, but employs an entirely different mechanism: premium support and competitive bidding. Seniors would enjoy exactly the same benefits that they do now, but along with the traditional Medicare program, they would enjoy the option of choosing among a selection of government-approved private insurance plans.

A repeal of Obamacare, Medicare cuts go to the solvency of the program -- not entirely new programs that have nothing to do with Medicare or its solvency.

House Republicans, led by Paul Ryan, passed something very similar to Wyden-Ryan in their 2012 budget. One notable difference are that the GOP budget targets Medicare growth of GDP plus 0.5 percent, just as the FY 2013 Obama budget does. (Wyden-Ryan targeted GDP plus 1 percent.) Importantly, as I noted above, the GOP budget repeals Obamacare, but preserves that law’s Medicare cuts.

Ryan's plan also calls for an overhaul of the program, offering beneficiaries a set amount of money that they would use toward buying a private plan or traditional Medicare.

Obamacare cuts to Medicare:

Yeah, I notice a very clear pattern here, OAW. When Ryan proposes targeted cuts in an attempt to save the program for future generations, it is pushing granny over a cliff. When Obama makes indiscriminate, across the board cuts to support a party pipe-dream -- it's a good and necessary thing. Just as I've said of you and other Democrats before; when an (R) does it, it's nefarious. When a (D) does it, it's necessary. This goes for unprovoked military action, Gitmo, torture, wiretapping, croneyism, etc...

I keep telling you, live by the CBO, die by the CBO:

According to the CBO:

Spending on the government’s major mandatory health care programs—Medicare, Medicaid, the Children’s Health Insurance Program, and health insurance subsidies to be provided through insurance exchanges—along with Social Security will increase from roughly 10 percent of GDP in 2011 to about 16 percent over the next 25 years. If revenues stay close to their average share of GDP for the past 40 years, that rise in spending will lead to rapidly growing budget deficits and surging federal debt.

The Obama Administration has been quite up front about the need to have young people sign up in order to make popular provisions like "No denial for pre-existing conditions" feasible. The individual mandate is the lynchpin to make the healthcare exchange work in what is fundamentally a private insurance based system. Which is precisely why the GOP supported it .... until it was implemented by a Dem. Hmmm ... there we go with that pattern thing again.

Get this out of your mind, OAW. The GOP never supported Obamacare. If you're going to cite the tired line on the individual mandate, you're going to pretend that I haven't already entirely disemboweled that argument here and elsewhere throughout this forum repeatedly.

"Overwhelming majority of small businesses" based on what? That little poll of 400 business owners that are all in the franchise game you mentioned?

Based on the friggin' entity that represents them. Otherwise, see above, you're just showing desperation in the argumentative line and once you realize what's in the health care overhaul you've been supporting, please acknowledge it to spare me yet another "I told you so" moment.

I didn't bloat anything. If you don't like the figure take it up with the Washington Post.

The Washington Post was the source I provided citing the study in the Journal Health Affairs indicating 48.6 million uninsured. The statement I quoted was; "Per Journal Health Affairs; When we talk about the Affordable Care Act, we mostly focus on the millions of Americans who will gain health insurance coverage. We talk less about the millions who will remain uninsured.

And there are a lot of them: 30 million Americans will not have coverage under Obamacare", according to a new analysis in the journal Health Affairs.

Originally Posted by OAW

Well it appears that I'm going to have to correct you again. let's review your original statement:"We've upended the entire health care industry to cover one-third [of] the uninsured when it's all said and done."

To which I said:

Originally Posted by ebuddy

I stand corrected. The proper statement would've been; little more than a third. But that's splitting hairs of course.

Now let's put your red pen away for a minute and take a look at your own claim under a microscope;

Now that's what YOU said. But what the numbers show is ...

- 54 million uninsured in 2010.

- ACA insures 32 million of those by 2019.

- Leaving 22 million uninsured in 2019.

32/54 = 0.5925925926

So we are looking at covering approximately 60% of the uninsured. I think that qualifies as substantially more than a " little more than a third".

- 48.6 million uninsured

- 30 million to remain uninsured

= 18.6 million insured or 38% insured after a complete upending of the entire health care industry. I repeat, a little more than a third and OAW splitting hairs in a desperate attempt to defend the indefensible.

From your own article ....

But why didn't you quote the ENTIRE statement OAW? Hmmm?

According to Google’s figures, if donations to all religious organizations are excluded, liberals give slightly more to charity than conservatives do. But Mr. Brooks says that if measuring by the percentage of income given, conservatives are more generous than liberals even to secular causes.

In any event, the characterizations I made in silver above ... admittedly exaggerated a smudge for for the sake of humor ... are views that are ROUTINELY expressed by conservatives. Often in this very forum.

Again, with all due respect; this qualifies as officially the most lame backpedal in 'NN history. Jon Stewart may be able to get away with this in bringing news to the distracted left, it doesn't carry the same satiric value coming from you. It's what you believe, OAW -- just stand behind it!

|

|

ebuddy

|

| |

|

|

|

|

|

|

|

Addicted to MacNN

Join Date: May 2001

Status:

Offline

|

|

Originally Posted by Shaddim

I tried to give you another chance, after 3 weeks on ignore, that was a mistake it seems.

You got that right! [Kevin Hart voice] Cause you gon' learn today!!! [/Kevin Hart voice]

Originally Posted by Shaddim

I linked the phrase but you brushed it off, I explained the rest, but that wasn't good enough and you wanted blood.

You see there are three bones of contention between us as a result of the recent claims you've made in the other thread. Those claims were:

1. You supposedly cited "Reuters or Drudge" for your unsubstantiated contention that TM was doing some drug called "lean".

2. I supposedly was "once making something up entirely" about the case. Even accused me of "lying" about it. And asked "why would I do that?"

3. And then I supposedly ducked the issue when you claimed "but you never gave an explanation, disappeared for a couple days, then continued on a different line of discussion as if it never happened."

I'm not making this stuff up. It's all here.

Now regarding #1, I challenged that and completely ripped it to shreds here. Again, not only did you provide no citation whatsoever for your claim you never even ONCE mentioned the words "Reuters" or "Drudge" at any point during the timeframe you were pushing that theory. You continued to insist that you did. And I called Bullsh*t! and dared you to " Prove me wrong!" by providing a link to a post where you actually said that. And as we both know that HAS NOT and WILL NOT happen ... because you can't. It simply does NOT EXIST. So when I mentioned above ... "don't think I forgot about that bit of "proof" that's still lacking." ... THAT is what I was talking about. And we both know that you already knew that because I provided a link to the post where this was spelled out. Which is why your response above talking about "I linked the phrase but you brushed it off" is such a transparent attempt to duck the fundamental issue because that link addressed #2. Did you really think you would be able to slip that past me?

Regarding #2 and #3, yeah you "linked the phrase" about that particular issue here. But where exactly did you "explain the rest"? Because the record shows that the only other things you said to me were to demand and apology [I'll address that little gem in a minute] otherwise you were going to put me on ignore here. And then to claim that I was "lying" and was "smearing" you here. So what exactly were you "explaining" related to #1, #2, or #3 above? In any event, I responded to you here where I reiterated how what I said that you accused me of "lying" about came straight from the court transcript. And for good measure, that post linked to my original post from July 29, 2013 where I had said the same thing, backed up by the court transcript itself, a mere 3 days after you initially made this claim. And yet there you are in Jan. 2014 steady claiming that I never addressed what you said and "continued on a different line of discussion as if it never happened". Uh huh. Ok.

Originally Posted by Shaddim

Then you decided to bring my family into it. What the f*ck is wrong with you? Is it my turn to start saying things about your wife? Your kids? At what point are you going to realize the friction in this (the walking on glass feeling in the PWL) is from your own temper?

First of all I never said anything about your family. I was talking about YOU. And how "your STATEMENTS are full of shi*t" ... for which you demanded an apology. And it'll be a cold day in hell before you EVER get one from me about this particular topic. And why should I when you make ... and then when challenged CONTINUE to make statements that are demonstrably, provably FALSE? Just see #1, #2, and #3 above! And let's add #4 from that thread as well when you claimed that the "local Assistant District Attorney who was visiting" told you that the old man who shot the guy for texting in the theater was "heavily bruised" because the younger man had "slugged him". Something else totally blown out of the water by the photo I provided of the old man showing no bruising whatsoever and all the witness statements saying the younger guy never hit the man. And then #5 when you claimed that the "Editor in Chief of a major newspaper" told you personally that they were " ordered not to discuss the matter, or allow a conversation on the subject" of Trayvon Martin's supposed "lean" use during the trial. But then you turn around in Jan. 2014 and claim that you got that info from a "Reuters or Drudge" article ... even said as much when you first made the claim ... but you have yet to produce the post in question where that actually happened. Not to mention the sheer stupidity of saying the major newspapers were supposedly blacklisting the story .... but you supposedly got it from REUTERS? Uh huh. Ok.

So like I said in the other thread ... "it's gotten to the point where your credibility is negligible at best." I just intimated about it before but since you want to continue talking sh*t I'll just come right out and say it. Given #4 and #5 it seems like you are developing a pattern of claiming some sort of "inside baseball" knowledge about whatever the controversial legal case du jour happens to be. Like I said ... it's awfully "convenient". So when you do that and then also make other utterly, completely false claims about my posts and yours ... especially when the thread history is readily available in black and white .... well let's just say that you are starting to come off like a POSER. Yeah. I said it. And one who is presumptuous enough to think he has some sort of knowledge about my emotional state at that.

Now what you could do at this point is simply tell the truth about #1, #2, and #3 above. Especially since the thread history is not your friend on this issue. But I imagine that would be too much like right for you at this stage in the game. So perhaps it would be better for you to just put me back on ignore. Assuming that you actually did before which considering the circumstances is not at all a given. That way you don't have to further embarrass yourself by resorting to the "angry" card because you can't produce a simple link to a post supporting your claims.

OAW

(

Last edited by OAW; Feb 8, 2014 at 07:43 PM.

)

|

|

|

| |

|

|

|

|

|

|

|

Professional Poster

Join Date: Dec 2006

Location: Maryland

Status:

Offline

|

|

Originally Posted by OAW

I appreciate your thoughtful response. So let's roll with that. You said the "Consumer Protections" can stay. That would be these ...

- Putting Information for Consumers Online.

- Prohibiting Denying Coverage of Children Based on Pre-Existing Conditions.

- Prohibiting Insurance Companies from Rescinding Coverage.

- Eliminating Lifetime Limits on Insurance Coverage.

- Regulating Annual Limits on Insurance Coverage.

- Appealing Insurance Company Decisions.

- Establishing Consumer Assistance Programs in the States.

- Prohibiting Discrimination Due to Pre-Existing Conditions or Gender.

- Eliminating Annual Limits on Insurance Coverage.

- Ensuring Coverage for Individuals Participating in Clinical Trials.

None of these provisions are in question from my standpoint. Concessions at the very least.

So how exactly would one provide these consumer protections ... especially the popular key provisions in blue ... without the individual and employer mandates for example that make such things feasible?

Can you explain why the individual and employer mandates are necessary for these consumer protections? I mean to answer your question directly, the individual mandate has nothing to do with these regulations.

- Premiums have been going up for decades. Often at double-digit rates. The rate of increase has actually slowed since the ACA was passed.

I suppose you didn't exactly read the source I provided last time we debated this issue, because had you done so you would know that the 40% increase for newly insured was compared to the projected costs increase for the same year without the ACA. In other words, the ACA is the cause of a 40% increase for newly insured coverage plans accounting for original rising costs. Were you simply not aware that insurance has gotten more expensive in the United States for new plans or are you simply ignoring that reality? Either's fine by me just want clarification on your position.

- It's dubious that less people are covered. Some in the individual market who purchased plans after the ACA was passed that didn't meet the new coverage standards had their policies cancelled.

Bzzt! Wrong again. Everyone who's policy didn't meet the standard got cancelled, the DOJ reversed course after getting called out for an outright law and told insurance companies they [b]could[b] continue old plans so long as they hadn't changed much since 2009. Not even the majority of policy holders were able to resume their old plans. Whether you blame the insurance companies or not is a moot point as the bottom line is we were outright lied to in the first place.

The "grandfather clause" only applied to those that existed prior to the law's passage. Which IMO was a mistake. It should have covered such policies until the the open enrollment period began for the Healthcare Exchange. In any event, most of those people will get a new, more comprehensive policy on the exchange.

At a 40% steeper price tag, whether paid by the policy holder or by me. Can you tell me why I am required to purchase maternity coverage by federal law?

You know ... something that actually covers things like hospitalization or medical procedures. Additionally, the Obama Administration extended the grandfathering period (subject to state insurance regulatory approval) for those affected policies. Then we have the millions that have signed up on the Exchange since the website was fixed.

Except that the website hasn't been fixed yet, and the backend ( you know the part that actually processes the policies) isn't even in testing yet.

A number that is only sure to grow exponentially as the end of the open enrollment period approaches.

What are you basing this assumption on?

- Jobs are disappearing based on what? Certainly not in the aggregate ....

You're grossly generalizing the situation. Are you trying to tell me the millions of people who're going to be forced to go part time or do so to get an entitlement check aren't going to have an impact on our economy?

- Small businesses are specifically exempt from the employer mandate provisions of the ACA.

So why in the world are we incentivizing them heavily not to grow?

I showed you mine ... now show me yours. IOW, I listed those aspects of the ACA that are already in effect. You say they've "been repeatedly refuted and severely undermined by independent, credible sources". So take some of the provisions I listed and then provide such sources that do so. I don't mean sources that are PREDICTING the sky falling at some point because of those provisions. I mean sources that demonstrate that those provisions are NOT actually in effect as the Obama Administration has claimed.

OAW

OAW,

You're certainly welcome to go back and look at the sources I provided previously in the other thread, where you can find a much better elaboration of the severe problems I've cited. If you need help finding them I'll be happy assist; my assumption is that you've simply forgotten that these claims were cited by credible sources.

You've not really shown me yours . You pretty much gave me an explanation of the pipe dream that is while ignoring with (un)intended consequences that the American public was kept out of the loop with. You know, things like "If you like your plan you can keep it" or "This will make costs go down and cover more people"

The costs haven't gone down - intact they've increased in the rate they're increasing, and less people are covered today than they were before this mess was forced down our throats by means of backroom deals and blatant bribes.

I'm asking you to show me these benefits from credible independent sources that show real, empirical, already happened datasets that show costs have dropped and more people in the United States have health coverage. I'm not asking you to explain the theory of why you think it could possibly work in the future.

(

Last edited by Snow-i; Feb 8, 2014 at 08:10 PM.

Reason: typos)

|

|

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Apr 2003

Location: 46 & 2

Status:

Offline

|

|

Originally Posted by OAW

*heavily distorted ramblings of a narcissistic ass*

Blah, blah, blah... just about everything you post in here (P&N) is so heavily colored and twisted that the only thing I can gather is that your mind actually warps anything coming into it. I've seen it before, generally with drug addicts and career fraudsters, they do that too. You manipulate and omit a little each time until you eventually change the substance of the topic to suit you. Whatever the reason, unconscious or intentional, I'm not going to run around doing your bidding, which would amount to me chasing my own tail. Go to therapy or eat a big shit taco, I don't care. Tell him what he's won, Johnny.

|

|

"Those who expect to reap the blessings of freedom must, like men, undergo the fatigue of supporting it."

- Thomas Paine

|

| |

|

|

|

|

|

|

|

Addicted to MacNN

Join Date: May 2001

Status:

Offline

|

|

^^^

Again. The thread history speaks for itself.

OAW

|

|

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Apr 2003

Location: 46 & 2

Status:

Offline

|

|

I'm sure you think it does.

|

|

"Those who expect to reap the blessings of freedom must, like men, undergo the fatigue of supporting it."

- Thomas Paine

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Jun 2001

Location: planning a comeback !

Status:

Offline

|

|

Originally Posted by OAW

^^^

Again. The thread history speaks for itself.

OAW

The only mad bro in this thread is you, OAW.

-t

|

|

|

| |

|

|

|

|

|

|

|

Addicted to MacNN

Join Date: May 2001

Status:

Offline

|

|

Originally Posted by Snow-i

Can you explain why the individual and employer mandates are necessary for these consumer protections? I mean to answer your question directly, the individual mandate has nothing to do with these regulations.

All of the consumer protections listed above in blue ... especially the ones dealing with pre-existing conditions ... can certainly be implemented at the stroke of a regulatory pen for sure. But we are still talking about the private insurance market with companies that are out to make a buck. So the costs of these protections would be passed onto customers in the form of astronomical premium hikes. Insurance is all about managing risk. The larger the risk pool ... the easier it is to manage that risk and make a reasonable ROI. So the purpose of the individual mandate is to enlarge the risk pool by including younger, healthier people that are statistically less likely to incur as many healthcare costs as older, sicker people. That way the expenses that the private insurance companies incur for when insuring people with pre-existing conditions or for imposing cost limits are absorbed by a larger group of customers. A truly progressive approach to this issue would be to go with a single payer model like most other industrialized nations. This has three primary benefits.

1. You can't create a larger risk pool than ALL US citizens. You can't press for a larger volume discount when negotiating pricing with healthcare providers, pharmaceutical companies, medical equipment suppliers, etc. than when you are purchasing for ALL US citizens.

2. You eliminate the portion of healthcare costs going towards the advertising, marketing, and profits of private companies. Private companies would then be free to compete in the supplemental insurance market.

3. You free up private enterprise of the burden of providing basic health insurance benefits for their employees. Thereby eliminating the "49'er effect" decried by the WSJ and cited by ebuddy.

In my view, it just makes more sense MATHEMATICALLY to go with a nationwide, single payer, non-profit health insurance system than the hodgepodge of 50 different private insurance markets along with a handful of government sponsored programs. But I'm also aware that this approach is politically untenable. So the "individual mandate" was an approach promoted by conservative think tanks (e.g. the Heritage Foundation) and promoted by GOP politicians as a "private insurance, market oriented" alternative to Hillarycare and its perceived " single payer, government sponsored" approach during the late 90s. Now my man ebuddy and I continue to go around and around about whether "Obamacare = Romneycare", about whether or not the private insurance orientation of the Healthcare Exchanges is a "conservative" idea, etc. A logical argument can be made either way when dealing with legislation as large and encompassing as the ACA nationally or Romneycare in MA. But one is hard pressed to make the argument that the "individual mandate" as a public policy concept was not a "conservative" idea. That it was not promoted by the GOP in terms of "individual responsibility", etc. Now again, we can all quibble about whether the "individual mandate" promoted by the GOP during the Clinton Administration was for comprehensive healthcare insurance vs catastrophic healthcare insurance. Regardless, the fact remains that the consumer protections in blue above cost money. And that money is either going to be paid by consumers in the form of private insurance company premiums, taxpayers in the form of government benefits or subsidies, or some combination of the two. The ACA as it is written involves some combination of the two with respect to the Healthcare Exchange. The "individual mandate" expands the risk pool on the Exchange ... so the increased costs borne by the consumer in the form of out-of-pocket premiums are minimized as much as possible.

Originally Posted by Snow-i

I suppose you didn't exactly read the source I provided last time we debated this issue, because had you done so you would know that the 40% increase for newly insured was compared to the projected costs increase for the same year without the ACA. In other words, the ACA is the cause of a 40% increase for newly insured coverage plansaccounting for original rising costs. Were you simply not aware that insurance has gotten more expensive in the United States for new plans or are you simply ignoring that reality? Either's fine by me just want clarification on your position.

It is true that new coverage plans in the individual market have seen a substantial premium increase as a result of the ACA. But this is by design. Not because the ACA intended to increase premiums for its own sake. Instead, it is because the ACA has mandated a minimum level of coverage that the private insurance companies had to provide. It's imposed standard, easy to understand "level" of benefits (i.e. Bronze, Silver, Gold, and Platinum) that the companies participating in the Exchange have to adhere to. Which is a good thing IMO ... because now consumers can know what they are signing up for without being buried under a mountain of legalese. It's amazing how people who will criticize the ACA because it's thousands of pages long seem to have no problem with the average consumer being inundated by all of this in a typical insurance policy. And then when the consumer has a health issue and they find out that the cut rate "insurance" policy s/he's been paying for doesn't even cover hospitalization, medical diagnostics, pharmaceuticals, therapy, etc. .... their attitude is essentially caveat emptor. In any event, the deal is that the private insurance companies gain a slew of potential new customers in exchange for competing on a level, easy to understand playing field. That being said, while the cost of the policies on the Healthcare Exchange has increased significantly beyond what existed in the individual market before as a result of more comprehensive coverage ... the out-of-pocket impact is expected to be minimized because of the premium subsidies that are available.

Originally Posted by Snow-i

Bzzt! Wrong again. Everyone who's policy didn't meet the standard got cancelled, the DOJ reversed course after getting called out for an outright law and told insurance companies they [b]could[b] continue old plans so long as they hadn't changed much since 2009. Not even the majority of policy holders were able to resume their old plans. Whether you blame the insurance companies or not is a moot point as the bottom line is we were outright lied to in the first place.

I don't have any info readily available on how many people have been able to continue with their old plans. Once the Obama Administration made this concession this issue has essentially dropped out of the news. In any event, I do put some onus on the insurance companies for continuing to sell a product that they new would be obsolete within a few years without full disclosure to the consumer. But as I've said before ... the administration also fumbled the ball on this one. The "grandfather clause" should have been until the open enrollment period in the Healthcare Exchange began from the jump ... not when the law was passed. So they bear the greater responsibility IMO.

Originally Posted by Snow-i

At a 40% steeper price tag, whether paid by the policy holder or by me. Can you tell me why I am required to purchase maternity coverage by federal law?

Well let me put it to you like this. And yes this is a rhetorical question because I'm not trying to get into your personal business. But are you currently insured? If so, is your insurance provided through your employer or purchased the individual market? The reason I ask is because there currently exists a huge discrepancy between the two markets when it comes to maternity coverage, contraception, preventive services, etc.

According to the New York Times, in 2011, 62 percent of plans in the private market did not cover maternity care at all. The National Women's Law Center, looking at a narrower slice of the population, found that in 2009, only "13% of the health plans available to a 30-year-old woman" across the country in the individual market covered maternity care—and "in the capital cities of nearly half of the states there was not a single plan available through eHealthInsurance.com that covered maternity care." Insurers were also allowed to reject pregnant women from coverage for having a pre-existing condition (pregnancy), and to exclude women who'd had a Cesarian section from coverage entirely (since they'd be at risk of needing another if they were to have another kid).

This was one of the critical ways the individual market differed from the employer-based one: More than half the plans in the individual market in 2010 did not meet the baseline "bronze-level" standards under the ACA, according to a 2012 study published in Health Affairs, while only 1 percent of plans in the employer-based market were similarly deficient "tin" plans. So to the extent that the ACA changes standards for insurance by adding maternity coverage, it does so almost entirely only within the individual market. Most group plans—such as the ones most employed people have—already cover maternity care. That means employed men and women have for years already been in the same situation with regard to pregnant women that people in individual-market plans will be starting in 2014.

Why Is Maternity Care Such an Issue for Obamacare Opponents? - Garance Franke-Ruta - The Atlantic

So what's happening here is that the individual healthcare insurance market is being brought more into parity with the larger employer based health insurance market. Per the Washington Post chart I posted above, 48% of Americans have health insurance through their employer. So all of these people ... male or female, young or old ... are ALREADY purchasing maternity coverage (and erectile dysfunction coverage for that matter) as part of a group policy whether they need it individually or not. When one signs up for health insurance at work you simply select "Individual", "Individual + Spouse", "Individual + Children", or "Family". Your gender doesn't matter. Nor does your age. Neither does the age or gender of your spouse or children. Neither do pre-exising conditions. That's simply how a group policy functions. And most reasonable people consider it to be superior in terms of cost and coverage than an individual policy. So there are legions of people right now with employer based health insurance who pose the same question you did in criticism of the ACA. I mean let's face it ... it's a popular and seemingly effective talking point going around in conservative circles. At least when talking amongst themselves. But at the same time these people are paying for "maternity care they don't need" or "erectile dysfunction care they don't need" essentially without complaint. And enjoying the comprehensive coverage benefits that a group policy affords. Granted, many may not have really thought it through with respect to how their own insurance coverage functions and are just regurgitating what they hear coming from conservative media pundits or politicians. So this part is NOT a rhetorical question. Once it is pointed out that this is simply how a group policy functions ... do you think any of these same people would advocate that the employer-based group policy they currently enjoy be restructured to function more like an individual policy?

Originally Posted by Snow-i

You're grossly generalizing the situation. Are you trying to tell me the millions of people who're going to be forced to go part time or do so to get an entitlement check aren't going to have an impact on our economy?

So why in the world are we incentivizing them heavily not to grow?

See #3 above. Personally, I think we should get private business out of providing basic health insurance coverage to their employees and make that federal, non-profit function. It's certainly not like the sun shines any brighter because I'm currently forking over money that I will have to expend anyway to a private company. Not only would this eliminate any disincentives to growth due to health insurance related regulations, it would also level the playing field internationally when competing against foreign companies that have no such cost burdens.

Originally Posted by Snow-i

You're certainly welcome to go back and look at the sources I provided previously in the other thread, where you can find a much better elaboration of the severe problems I've cited. If you need help finding them I'll be happy assist; my assumption is that you've simply forgotten that these claims were cited by credible sources.

No need to recite anything you've posted before. A simple link to a relevant post will suffice. I'd be happy to look it over and we can go from there.

OAW

PS: I appreciate the constructive discourse. The number of people around here who seem capable of doing so across the ideological spectrum is sadly decreasing.

(

Last edited by OAW; Feb 10, 2014 at 06:57 PM.

)

|

|

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Jun 2001

Location: planning a comeback !

Status:

Offline

|

|

So, another day, another "delay".

When can we finally enjoy the ObamaCare "success" in its full glory ?

-t

|

|

|

| |

|

|

|

|

|

|

|

Posting Junkie

Join Date: Aug 2003

Location: midwest

Status:

Offline

|

|

Yup -- the Law of the Land® gets more ridiculous by the day. A delay in the business mandate of an additional year now to 2016, ironically while mired in debate with OAW who insists this problem is a figment of opponents' imagination.

What I don't understand is if an aspect of a law is so injurious that it must be addressed, how is a delay the solution to this injury? In other words, these 27 delays or whatever we're at now are going to be as much an issue in 2016 as they are today. What, other than the most cynical notion imaginable; a delay for the Presidential election, do these delays effectively accomplish? Are the American people really as stupid as this Administration must assume they are?

I mean, how is any of this even legal?

|

|

ebuddy

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Jun 2001

Location: planning a comeback !

Status:

Offline

|

|

It's legal because Obama says so.

Stop questioning his wisdom and pure motives.

-t

|

|

|

| |

|

|

|

|

|

|

|

Professional Poster

Join Date: Dec 2006

Location: Maryland

Status:

Offline

|

|

Originally Posted by OAW

All of the consumer protections listed above in blue ... especially the ones dealing with pre-existing conditions ... can certainly be implemented at the stroke of a regulatory pen for sure. But we are still talking about the private insurance market with companies that are out to make a buck. So the costs of these protections would be passed onto customers in the form of astronomical premium hikes. Insurance is all about managing risk. The larger the risk pool ... the easier it is to manage that risk and make a reasonable ROI. So the purpose of the individual mandate is to enlarge the risk pool by including younger, healthier people that are statistically less likely to incur as many healthcare costs as older, sicker people. That way the expenses that the private insurance companies incur for when insuring people with pre-existing conditions or for imposing cost limits are absorbed by a larger group of customers. A truly progressive approach to this issue would be to go with a single payer model like most other industrialized nations. This has three primary benefits.

1. You can't create a larger risk pool than ALL US citizens. You can't press for a larger volume discount when negotiating pricing with healthcare providers, pharmaceutical companies, medical equipment suppliers, etc. than when you are purchasing for ALL US citizens.

2. You eliminate the portion of healthcare costs going towards the advertising, marketing, and profits of private companies. Private companies would then be free to compete in the supplemental insurance market.

3. You free up private enterprise of the burden of providing basic health insurance benefits for their employees. Thereby eliminating the "49'er effect" decried by the WSJ and cited by ebuddy.

This is communism, brother. :/ I'm still sitting here waiting for you to show me the improvements to all the things you say it's gonna do. I've shown you it's had the opposite effect.

In my view, it just makes more sense MATHEMATICALLY to go with a nationwide, single payer, non-profit health insurance system than the hodgepodge of 50 different private insurance markets along with a handful of government sponsored programs

Why don't we just remove the big-biz friendly regulations causing those 50 different markets and allow for cross-state competition? Why do we need a mandate to fund consumer protections that can easily be addressed by the free market?

. But I'm also aware that this approach is politically untenable.

You mean economically untenable. Which parts of ObamaCare are saving us money as promised?

So the "individual mandate" was an approach promoted by conservative think tanks

You've been debunked in this notion no less than three times already, and last I checked failed to address any of the rebuttals presented against you.

Originally Posted by OAW

It is true that new coverage plans in the individual market have seen a substantial premium increase as a result of the ACA. But this is by design.

Originally Posted by OAW

The rate of increase has actually slowed since the ACA was passed.

Which is it man? You're openly contradicting yourself in successive posts to me now.

Not because the ACA intended to increase premiums for its own sake. Instead, it is because the ACA has mandated a minimum level of coverage that the private insurance companies had to provide. It's imposed standard, easy to understand "level" of benefits (i.e. Bronze, Silver, Gold, and Platinum) that the companies participating in the Exchange have to adhere to. Which is a good thing IMO ... because now consumers can know what they are signing up for without being buried under a mountain of legalese. It's amazing how people who will criticize the ACA because it's thousands of pages long seem to have no problem with the average consumer being inundated by all of this in a typical insurance policy.

What's your justification for forcing me to buy Maternity and rehab insurance? I don't need either and can't afford things I have absolutely no need for.

So you think a mountain of codified law is better than a mountain of codified insurance documents?

I know what I'm signing up for, but I don't want it. It doesn't fit me or my lifestyle. Why do I have to buy an inferior policy than what I could before?

And then when the consumer has a health issue and they find out that the cut rate "insurance" policy s/he's been paying for doesn't even cover hospitalization, medical diagnostics, pharmaceuticals, therapy, etc. .... their attitude is essentially caveat emptor. In any event, the deal is that the private insurance companies gain a slew of potential new customers in exchange for competing on a level, easy to understand playing field. That being said, while the cost of the policies on the Healthcare Exchange has increased significantly beyond what existed in the individual market before as a result of more comprehensive coverage ... the out-of-pocket impact is expected to be minimized because of the premium subsidies that are available.

You're rambling at this point. Show me something that backs up your claims of improvement. All you have right now is a pipe dream.

I don't have any info readily available on how many people have been able to continue with their old plans.

So you were talking out of your ass before?

Once the Obama Administration made this concession this issue has essentially dropped out of the news. In any event, I do put some onus on the insurance companies for continuing to sell a product that they new would be obsolete within a few years without full disclosure to the consumer. But as I've said before ... the administration also fumbled the ball on this one. The "grandfather clause" should have been until the open enrollment period in the Healthcare Exchange began from the jump ... not when the law was passed. So they bear the greater responsibility IMO.

This does not suggest a little bit to you that this Administration has no idea what it's doing? I mean, as a project manager myself I find it incredibly improbable that no one asked these questions early on. It's not like this was hard to see coming when he got up and said "If you like your plan you can keep it." He didn't have anyone check to see if that was actually the case? Or was that mountain of paper too much for him to be well versed about?

Well let me put it to you like this. And yes this is a rhetorical question because I'm not trying to get into your personal business. But are you currently insured? If so, is your insurance provided through your employer or purchased the individual market? The reason I ask is because there currently exists a huge discrepancy between the two markets when it comes to maternity coverage, contraception, preventive services, etc.

Considering that you chimed in on the thread that we went over my specific situation, I'm a bit dumbfounded that you ask me this question. Do you not remember our exchange in the other thread?

So what's happening here is that the individual healthcare insurance market is being brought more into parity with the larger employer based health insurance market. Per the Washington Post chart I posted above, 48% of Americans have health insurance through their employer. So all of these people ... male or female, young or old ... are ALREADY purchasing maternity coverage (and erectile dysfunction coverage for that matter) as part of a group policy whether they need it individually or not.

This is hogwash dude. How did you get to all of those people already purchasing maternity coverage?

When one signs up for health insurance at work you simply select "Individual", "Individual + Spouse", "Individual + Children", or "Family". Your gender doesn't matter. Nor does your age. Neither does the age or gender of your spouse or children. Neither do pre-exising conditions. That's simply how a group policy functions. And most reasonable people consider it to be superior in terms of cost and coverage than an individual policy. So there are legions of people right now with employer based health insurance who pose the same question you did in criticism of the ACA. I mean let's face it ... it's a popular and seemingly effective talking point going around in conservative circles. At least when talking amongst themselves. But at the same time these people are paying for "maternity care they don't need" or "erectile dysfunction care they don't need" essentially without complaint. And enjoying the comprehensive coverage benefits that a group policy affords. Granted, many may not have really thought it through with respect to how their own insurance coverage functions and are just regurgitating what they hear coming from conservative media pundits or politicians. So this part is NOT a rhetorical question. Once it is pointed out that this is simply how a group policy functions ... do you think any of these same people would advocate that the employer-based group policy they currently enjoy be restructured to function more like an individual policy?

This entire line of reasoning is based on the faulty premise that everyone always purchases maternity coverage. I never have. And never will.

See #3 above. Personally, I think we should get private business out of providing basic health insurance coverage to their employees and make that federal, non-profit function.

Where is this part in the constitution again?

It's certainly not like the sun shines any brighter because I'm currently forking over money that I will have to expend anyway to a private company.

Yeah but I usually fork that money over towards my costs, not older people's. Now I have to expend 40% more of it to cover others than myself.

Not only would this eliminate any disincentives to growth due to health insurance related regulations, it would also level the playing field internationally when competing against foreign companies that have no such cost burdens.

You've yet to show me anything other than a leftist pipe dream on the improvements you're claiming the ACA has. Show me these improvements today, 3 years after the laws passage and after several public bungles. Don't you think as a taxpayer I have a right to see where my money is being invested?

I see a lot of hypotheticals and justifications but I don't see where you're showing the me the improvements you're claiming the ACA is having on us. Is it....you know....just not yet? In a few years things will be better or is this law supposed to make our healthcare system better today?

When can I expect to see where my extra 40% for maternity coverage is going?

PS: I appreciate the constructive discourse. The number of people around here who seem capable of doing so across the ideological spectrum is sadly decreasing.

Always

|

|

|

| |

|

|

|

|

|

|

|

Professional Poster

Join Date: Dec 2006

Location: Maryland

Status:

Offline

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

Clinically Insane

Join Date: Apr 2003

Location: 46 & 2

Status:

Offline

|

|

|

|

|

"Those who expect to reap the blessings of freedom must, like men, undergo the fatigue of supporting it."

- Thomas Paine

|

| |

|

|

|

|

|

|

|

Addicted to MacNN

Join Date: May 2001

Status:

Offline

|

|

Originally Posted by Snow-i

This is communism, brother.

Actually a single-payer healthcare insurance system is NOT "communism". Communism advocates the elimination of the concept of private property. It advocates public or "communal" ownership of the means of production. If the existing Medicare system were expanded to cover all US citizens and not just the elderly that would in no way, shape, fashion, or form constitute "communism". Hospitals, doctors, pharmaceutical companies, and other healthcare providers would still be private entities. Let's not go using such terms inaccurately ok?

Originally Posted by Snow-i

Why don't we just remove the big-biz friendly regulations causing those 50 different markets and allow for cross-state competition? Why do we need a mandate to fund consumer protections that can easily be addressed by the free market?

I could have sworn I just said that! In any event, let me be clear. It's no secret that I would have preferred a single-payer system. Like about half of the people who polls show don't favor Obamacare in its current form. That being said, since that was unachievable I would have much preferred a private system where health insurance regulation was performed at the federal instead of the state level. I just see no justification for sticking with a system that forces a large insurance company to have to comply with 50 different sets of regulations. As an IT project manager I see firsthand the insanity of this when implementing computer systems. Just look at healthcare.gov. It's trying to accommodate the 38 states that chose not to build their own marketplace. And comply with 38 different sets of regulations. So it's certainly no surprise that the vast majority of those states that opted to build their own website and only had to comply with a single set of regulations did so successfully, at much lower cost, and without all the implementation issues. The current state-by-state regulatory regime is unnecessarily costly, burdensome, and anti-competitive. Unfortunately, there are those in our political system who recoil in knee-jerk fashion at the very notion of a "national" or "federal" anything. "Leave it to the states!" they say. "Federal takeover of healthcare!" they say. And "they" are certainly not coming from the left.

Originally Posted by Snow-i

You've been debunked in this notion no less than three times already, and last I checked failed to address any of the rebuttals presented against you.

You may call it "debunked". And I call that the "Who are you going to believe? Me or your lying eyes?" argument. From the original document itself ....

THE HERITAGE PLAN

The fundamental defects of the existing system and the serious flaws in most solutions to the problem of uninsurance has led The Heritage Foundation to propose a national health system based on very different foundations. Developed in detail in a new monograph, A National Health System for America, the Heritage plan aims at achieving four related objectives:

- All citizens should be guaranteed universal access to affordable health care.

- The inflationary pressures in the health industry should be brought under control.

- Direct and indirect government assistance should be concentrated on those who need it most. * *

- A reformed system should encourage greater innovation in the delivery of health care.

The Heritage plan has several key components:

.

.

.

2) Mandate all households to obtain adequate insurance.

Many states now require passengers in automobiles to wear seat-belts for their own protection. Many others require anybody driving a car to have liability insurance. But neither the federal government nor any state requires all households to protect themselves from the potentially catastrophic costs of a serious accident or illness. Under the Heritage plan, there would be such a requirement.